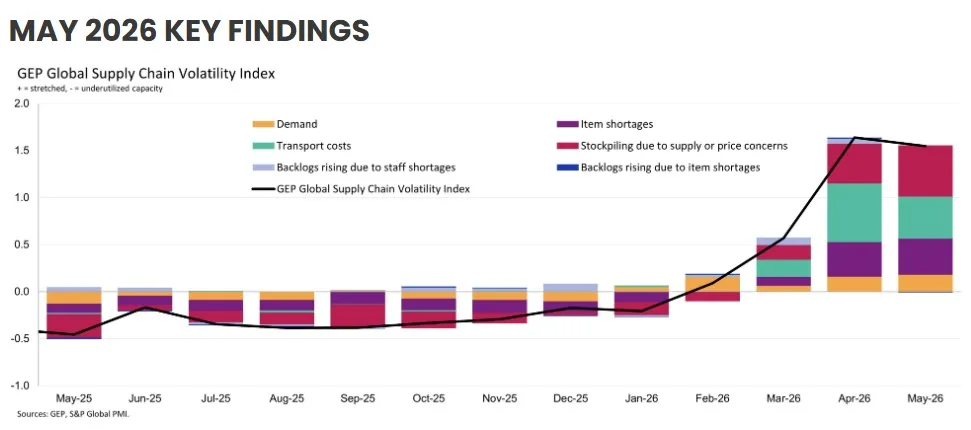

New data from the GEP Global Supply Chain Volatility Index shows manufacturers across North America, Europe and Asia are accelerating inventory build-ups and front-loading purchases as concerns over inflation, shortages and supply chain disruption intensify, raising questions about supply chain resilience in the second half of 2026.

- Key Regional Findings May 2026

- Manufacturers Accelerate Inventory Build-Up to Mitigate Risk

- Supply Shortages Continue to Worsen Across Global Markets

- North America Records Highest Supply Chain Pressure Since 2022

- Procurement Teams Face a Potential Demand Correction

- About the GEP Global Supply Chain Volatility Index

Key Regional Findings May 2026

Global supply chains remained under significant pressure in May as manufacturers increased purchasing activity and expanded safety stock levels in anticipation of higher costs and potential supply disruptions later this year, according to the latest GEP Global Supply Chain Volatility Index.

The index, which draws on survey data from approximately 27,000 businesses worldwide, indicates that companies are taking proactive measures to secure supply and manage inflation risks, driving a sharp increase in inventory accumulation and raw material purchasing.

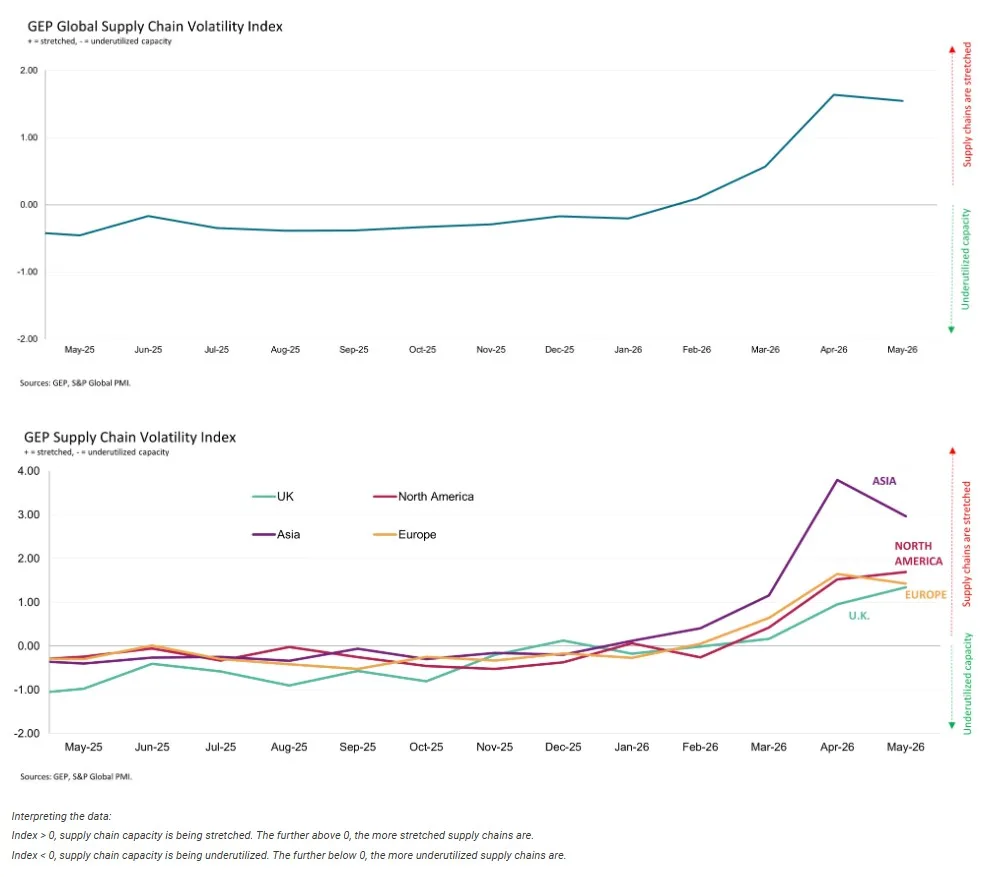

- ASIA: Index fell from 3.79 to 2.96, signalling a slight easing of pressures versus April. Nonetheless, the index was indicative of significant supply chain stress for Asian manufacturers.

- NORTH AMERICA: Index rose to 1.69, from 1.52, its highest level since August 2022. Stronger purchasing activity, particularly in the U.S., and greater stockpiling, drove the rise in supplier capacity pressures.

- EUROPE: Index fell to 1.43, from 1.64, as factory purchasing volumes across the continent were tapered. This reflected fresh signs of weakness in the German and French manufacturing economies.

- U.K.: Index rises to three-and-a-half year high of 1.34, up from 0.96 in April, pointing to greater capacity constraints for suppliers used by U.K. manufacturers.

Manufacturers Accelerate Inventory Build-Up to Mitigate Risk

Safety stockpiling reached its highest level since January 2023, reflecting a growing trend among manufacturers to build inventory buffers against anticipated price increases and supply constraints.

The increase in precautionary purchasing pushed global demand for raw materials, commodities and intermediate goods to its strongest level since March 2022. Manufacturers across Asia, North America and Europe reported more aggressive inventory strategies as geopolitical tensions and supply uncertainty continued to influence procurement decisions.

The data suggests businesses are prioritising supply assurance over inventory optimisation, a trend reminiscent of behaviours seen during the height of the 2021–2023 supply chain crisis.

Supply Shortages Continue to Worsen Across Global Markets

Compounding the situation, material shortages intensified in May, reaching their highest level in three-and-a-half years.

The combination of constrained supply and stockpile-driven demand is placing additional pressure on suppliers and contributing to rising factory-gate costs. Elevated transportation expenses have further amplified supply chain challenges, despite some easing from the record highs recorded in April.

May marked the third consecutive month in which stockpiling activity, shortages and transportation costs all remained elevated simultaneously — a pattern rarely observed outside major supply chain disruptions.

According to GEP, similar conditions in the past have often been followed by a period of correction as inventory levels normalise and purchasing activity slows.

North America Records Highest Supply Chain Pressure Since 2022

Regional data highlighted growing pressure on supplier capacity, particularly in North America.

The North American index rose to 1.69 in May, its highest reading since August 2022, driven by stronger purchasing activity and increased inventory accumulation, particularly among U.S. manufacturers.

Asia remained the most strained region globally despite a modest easing in conditions. The regional index fell from 3.79 to 2.96, although manufacturers continued to report significant supply chain stress. Increased purchasing activity was reported across several key manufacturing economies, including Japan, India, South Korea and Taiwan.

In Europe, supply chain pressures eased slightly as procurement activity slowed, reflecting continued weakness in major manufacturing economies such as Germany and France. However, the UK diverged from the broader European trend, with its index climbing to a three-and-a-half-year high as supplier capacity constraints intensified.

Procurement Teams Face a Potential Demand Correction

The latest findings suggest that current procurement activity may represent a temporary surge rather than a sustained increase in underlying demand.

John Piatek, Vice President, Consulting at GEP, said the current wave of purchasing reflects efforts by businesses to limit exposure to future inflationary pressures.

“The path for inflation is already being set, and companies are trying to limit the damage,” said Piatek.

“The surge in purchasing we saw in April and May is likely temporary. Once companies have built inventory, they and their customers will pull back, which means supply chain pressures may ease.”

He added that inventory drawdowns later in the year could contribute to softer economic conditions and reduced purchasing volumes across supply chains.

“But, even if the Strait of Hormuz is opened fully, economic conditions will likely weaken in the second half of the year as companies will pull back on their input purchasing to draw down the inventories they’ve built up.”

About the GEP Global Supply Chain Volatility Index

The GEP Global Supply Chain Volatility Index is produced by S&P Global and GEP. It is derived from S&P Global’s PMI® surveys, sent to companies in over 40 countries, totalling around 27,000 companies.

The headline figure is a weighted sum of six sub-indices derived from PMI data, PMI Comments Trackers and PMI Commodity Price & Supply Indicators compiled by S&P Global.

This article was produced by the editorial team at North America Outlook and published as part of the Outlook Publishing global network of B2B industry magazines.

Outlook Publishing delivers industry insights, company stories, and sector coverage across manufacturing, mining, construction, healthcare, supply chains, food production, and sustainability.

North America Outlook provides ongoing coverage of organisations and developments shaping industries across North America.